Crocs Updates Dec 2024

An update and insight about Crocs

Crocs’ stock price has had an over 30% pullback from its high of $150 to below $100 per share since its most recent earnings release, even though its earnings for the quarter beat the street expectation by over 15%. The main reason for the decline is that the Hey Dude brand’s revenue continues to decline, contracting 17% YoY. HEYDUDE’s wholesale revenues were down 23% and DTC revenues were down 9%. The company acknowledges that it will take longer than it had initially planned for the business to turn the corner. However, Wall Street has lost its patience.

It has been about one year since Crocs's management started communicating the struggle with Hey Dude's revenue. In 2022, the Hey Dude brand’s revenue skyrocketed to nearly $1B from about $250M two years ago. However, about 60% of these revenues came from the wholesale channel. Many wholesalers were buying Hey Dude at wholesale prices while selling them online at third-party (mainly Amazon) retail prices. That is breaching the Hey Dude contract for not selling on retail e-commerce websites.

Since then, Hey Dude has been shutting down over 50% of wholesale accounts to protect such black market transactions. This caused the revenue to decline since the beginning of the year. But the goal and the expectation is to bring the brand back to a growth trajectory by the end of 2024. Unfortunately, this seems to be taking longer than expected, and apparently, the street is out of patience.

Why does the market react so negatively?

The market probably lost its patience or faith in the turnaround for the Hey Dude Brand. It has been a year since Crocs has been working on the Hey Dude challenge. For Wall Street, one year is long enough and the ship should have been turned. It has been a year since the management communicated the problem and has had dedicated efforts and resources to make the turnaround happen, but it hasn’t happened yet. Unfortunately, measured by revenue growth, it apparently would take longer and the street is very frustrated, and thus a big sellout.

What do I see

Zoom in view - Look at the Hey Dude Brand specifically

Before diving into a bigger picture of Crocs as a company, let me first zoom in to understand what are the reasons for Hey Dude’s revenue decline. Instead of just saying that the revenue wasn’t able to return to growth, we should understand why that happened.

As explained by one of the Q&A during the earnings call, the management explained that there is a shift in Hey Dude’s marketing strategy. It is changing from a performance-driven marketing strategy (focusing on conversion) to a brand-focused strategy. The shift is due to the ROI from performance marketing not reaching the desired expectation of the management team. So it starts to shift to brand marketing campaigns, mainly through influencers, the same playbooks Crocs brand has successfully applied for years.

This year, Hey Dude signed two influencers, Jelly Roll and Sydney Sweeney. During its launch days, the Hey Dude brand emerged as the number one global key account on TikTok, definitely a successful accomplishment. I also consider this a very rational and disciplined marketing decision, focusing on the efficiency and the long-term return of marketing spend rather than chasing purely conversion-focused marketing spend when the ROI doesn't reach expectations.

So in the short term, such a shift of marketing focus from performance-focused to brand-focused would reduce sales. But to me, it shows the discipline and rationality of very good marketers. Terence Riley, Hey Dude’s Chief, is a very savvy marketer who was previously Crocs’s CMO and Stanley Cups’ president. We will discuss him more in the following. In short, he is not chasing growth at any cost of marketing but focuses on the long term to build up a loyal customer base.

Although Hey Dude's revenue hasn’t turned to growth yet, the brand has made a lot of progress with its profitability and inventory efficiency.

Profitability: by shutting down these grey wholesale channels and elevating ASP (average sale price). Hey Dude’s gross margin increased by 510 basis points YoY to 47.9% from 42.8% last year. This is 290 extra basis points improvements than the Crocs brand and about 400 basis points more than other apparel companies I tracked. This alone translates to an increase of $40M increase of gross profit. For most businesses that generate close to a $1B run rate within a competitive market, it is very hard to increase their gross margin by over 200-300 basis points. Operating margin could be improved by cutting down costs and reducing headcounts. But it’s very hard to charge more for the same products. However, the brand can increase gross margin by over 500 basis points, which is a very impressive accomplishment by itself.

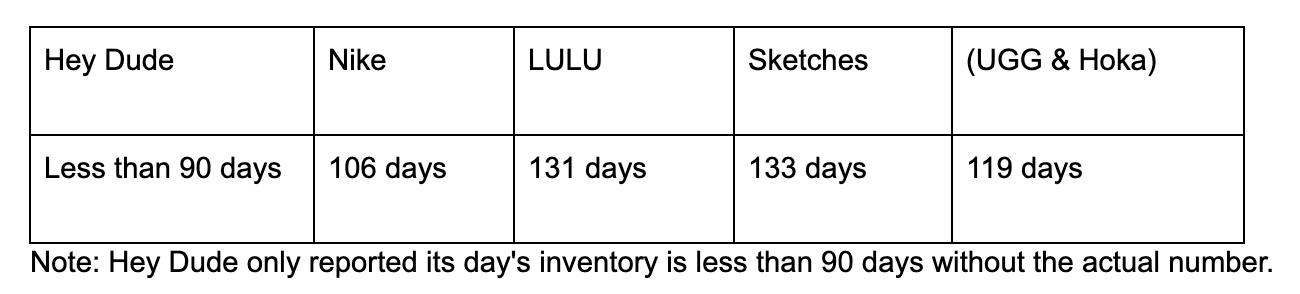

Inventory Efficiency: improving inventory turns to four times a year by opening premium outlet stores. Reducing inventory turns to four times a year is equivalent to having days in inventory to be less than 90 days per year, so 4 turns per year. This is a very critical metric to measure the efficiency of apparel & retail companies because inventory takes cash flow. Getting inventory to be less than 90 days is an extraordinary accomplishment. Just provide some comparison, no other company can reach below 100 days of inventory among all brands while Crocs is at 81 days. (If you are not familiar with the metric, just know the lower, the better).

With the disciplined focus, the management is essentially focused more on improving the efficiency and profitability of the brand, rather than just the top line. From this lens, they have made very significant progress.

Zoom out view - Look at the company as a whole.

Zooming out the Hey Dude brand, I want to share a bit more thoughts or views about Crocs as a company. After all, we don’t invest in Hey Dude but the whole company (Crocs and Hey Dude brand combined). These are the three main reasons that we deploy more capital into the company.

Disciplined and rational management with a phenomenal track record and a long-term focus. In addition,

CEO holds very significant company shares.

They can recruit amazing talents.

Superior capital efficiency

Very attractive valuation, with small downside risk.

Disciplined and rational management with significant insider holdings

Andrew Rees is the CEO of Crocs, taking the role in 2014 from a senior consultant role. In 2014, Crocs was barely profitable, with ~1B revenue, a 2% operating margin, and negative free cash flow. 10 years later, the company is generating $4B generating revenue, close to $ 1B in free cash flow, and an operating margin of over 25%! So Andrew has some successful turnaround experiences he could brag about. But note that it took 10 years and in the first 3 years the progress was hardly noticeable. The same would probably apply to the Hey Dude brand.

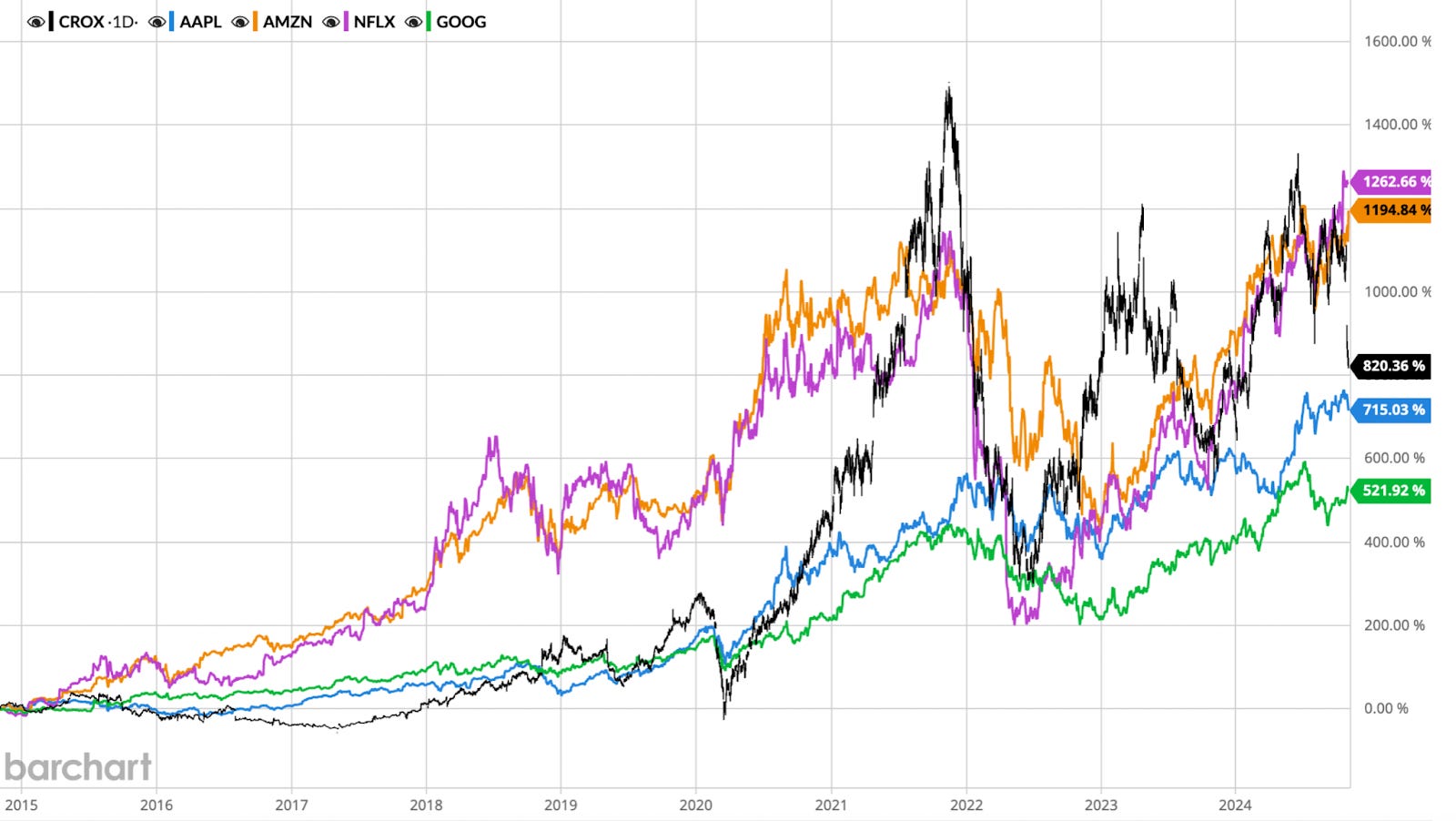

Since Andrew took the CEO role in 2014, Crocs' revenue has grown over 300%, even excluding the acquisition of Hey Dude, becoming one of the fastest-growing companies in the past 10 years. Its stock performance has significantly outperformed Google and Apple (even after the most recent 30%+ pullbacks. If not accounting for the most recent 30% pullback, Crocs had over 1000% return and is at the same level as Amazon and Netflix). There’s no doubt that Covid gave Crocs some tailwinds. However, to achieve such success, one cannot be just lucky, but needs also to be capable of taking advantage of the trends. By any measure, we need to give due credit to Andrew.

Andrew is a very talented marketer and disciplined capital allocator. You can tell from the company’s superior capital efficiency (more discussion below). Croc’s success as a consumer-facing company relies not only on its good products but also on its very efficient marketing campaigns and impressive capital allocation decisions.

Last but not least, Andrew holds over $110M Crocs Stock. This significantly helps align his interests with shareholders. BTW - before writing this, I didn’t know he was that rich ;-)

Terence Riley is the President of Hey Dude. He was Crocs’ CMO from 2013 to 2020. So he partnered with Andrew for a long period before 2020. While Covid gave the casual shoe brand a significant boost, Terence’s marketing talent contributed significantly to Crocs’ success far before Covid, turning it from an ugly shoe brand to a fashion brand that attracted a significant amount of loyal female customers. Over 60% of Crocs buyers are female. In 2020, Terrence took Stanley's presidency role. Within 4 years, he increased Staneley’s revenue by 10x, from $70M to $700M.

In early 2024, Terence came back to Corcs to take Hey Dude’s presidency. Yes, that’s right, the marketing genius behind the successful story of Stanley Cup & Crocs is the same person. If he just succeeded once, you could argue it’s luck. If he did it twice (Crocs & Stanley), something must be behind him. There are tons of research & interviews (an 8-minute video by Forbs & Ross Business School, highly recommended) and case studies from top business schools to understand Terence’s success and strategy. But the most important thing for us as investors is he is now the president of the Hey Dude brand and playing his marketing magic. I have watched many of Terence’s interviews. He is a very rational and disciplined marketer with a sincere attitude toward his products and consumers. One of my favorite Riley quotes is: “A good marketer is chasing people's hearts, not their wallets ”

[News - New talent joined Crocs]

Crocs’s management recruited Steven Smith to join Crocs as head of design in Nov 2024. You may not have heard his name but he is the designer behind the famous Adidas Yeezy, the one promoted by Kanye West (now known as Ye). Steven is very well-known and respected in the shoe design industry and has designed very successful silhouettes for Adidas, Nike, Reebok, and New Balance. The Yeezy line with Adidas is a huge hit, which generated $2B in revenue for Adidas in 2022.

Convincing design profiles like Steven to join the company itself is an achievement for the management team of Crocs. What’s more interesting to me is the fact that Steven decided to join Crocs. Most people I talked with consider Crocs shoes to be nothing but an ugly pair with 13 holes. However, Crocs has been very active in working with many designers and experimenting with different designs. A couple of these are newly released designer shoes. What’s more, Crocs’ fabric - a foam called Croslite, is very easy to shape and thus creates new designs while maintaining its comfortable functionalities. By no means I am a designer, but designers with such high caliber to head up Crocs’s design is a very solid endorsement of the company’s design and innovative potential. Lastly, Steven is heading up the design function of both Crocs and Hey Dude brands. Given his track record and success, that’s another reason to increase some confidence in the Hey Dude brand’s turnaround.

I spent more time covering the management team. Over time, I found management is a source of "insight" that is critical but hard to identify. They are hard to measure using numbers, and thus often ignored by people applying first level thinking.

Superior Capital Efficiency

Crocs as a shoe company has the capital efficiency of a software company, or even more efficient. Measured by return on tangible assets, Crocs is almost 2X of Google and 3X of Meta!

Gross Margin 58%

Operating Margin 25%.

ROIC (return on invested capital) at 23%.

Return on Tangible assets (EBIT/Tangible assets): 136%. (Google: 71%, Meta: 56%)

Not only does Crocs have a very high return on tangible assets, but it also has a superior free cashflow margin at above 20%, outperforming Google and any other apparel companies.

Free Cash Flow margin at 23.1% (Google: 16%, Meta: 33%; for apparel companies, Sketchers: 3.6%, Lululemon: 17%, Nike: 14%)

Free cash flow is the ultimate measure of profitability. Also, it’s a cash measurement so companies usually cannot play accounting tricks like earnings. Having a free cash flow margin of over 20% is very impressive for an apparel company. This means for every $100 revenue made, $23 would be left as that is freely disposable (Free Cash Flow) after both operational expenses (including marketing) and capital expenditures.

Crocs’s high capital efficiency is due to a couple of factors:

Strong brand loyalties and engagement

Efficient marketing campaigns with loyal customers

Very low capital expenditures relative to its cash flow from operation. Crocs spent less than 10% of its cash from operations as capital expenditure.

I recently had a chance to read and learn more about Skechers (SKX). Sketchers generated about $8.5B in revenue per year, a little over 2X than that of Crocs. However, during the same period, Crocs’s FCF iwas$940M while Sketcher only generated $400M. So while Crocs generated less than half of SKX revenue, it produced more than twice of FCF with its superior operating efficiency and low capital expenditures.

Valuation

With Crocs stock now trading at ~$100 per share, it is trading at less than 7X of Free Cash Flow (FCF), or equivalently, over 15% FCF yield. This means if we deposit our money into a “Crocs” bank, it would yield over 15% annually. One would assume this is a business that has a very high risk of going bankrupt. However, Crocs is a very stable and growing business. Although Crocs’s total revenue growth has been slowing down, largely due to Hey Dude’s negative growth, its profitability and cash generation have been consistently growing. This is driven by the company’s continuing improvements in its operation and disciplined spending. Crocs’s trailing twelve-month free cash flow growth is 15% YoY. This is on top of a 60% Free cash flow growth in 2023. Its FCF growth is mainly driven by the increase in gross margin and improving Days Inventory.

Gross margin growth: Crocs’s gross margin grew by over 4% from 55.6% to 59.6% YoY. For a $4B company, this translates to $160M gross profit. The increase is due to product mix change and lower transportation costs. During the same period, Nike, Lululemon, and Sketchers all grew gross margins by ~1%.

Improved inventory efficiency, measured by Days Inventory. During the most recent quarter, Crocs’s Days Inventory reached below 80 days, indicating over 4x inventory turnover rate per year. This significantly improved its efficiency of working capital and contributed to its free cash flow. As a comparison, here is the Days Inventory for other apparel retailers Sketcher: 133 days, Lululemon: 130 days, Nike: 106 days. (The lower the number, the more efficient a company is with its inventory)

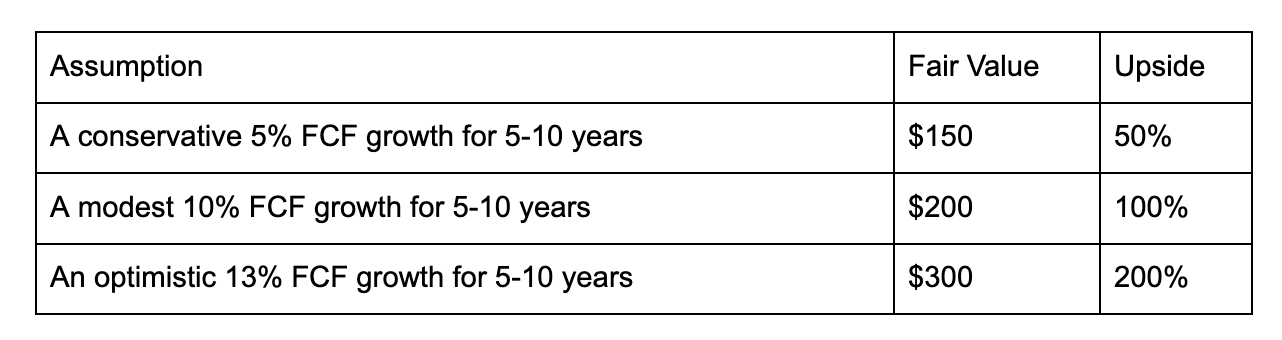

In a very conservative case, assuming FCF grows at 5% per year, the valuation would be around $150-$160 per share. Indicating a 50% upside potential.

Crocs valuation estimate

With its current FCF growth of 15% YoY, I think the conservative or modest scenario to play out is very achievable.

I am also a big fan of using reverse DCF to look at valuation. Reverse DCF is, as the name suggests, to calculate what growth trajectory would be required for the company to justify its current share price. When Crocs’s share price is at $100, its implied earning or free cash flow growth rate is a negative of 2%-3% in the next 5-10 years. Even with Hey Dude's revenue decline, the Crocs Inc. company still managed to grow its free cash flow by 15% YoY and revenue per share grew by ~5% in the past few quarters. As a well-known consumer brand, Crocs is unlikely to experience a dramatic revenue decline shortly. So a negative implied revenue growth seems overly pessimistic.

Competition

With Crocs’s revenue reaching over $3B, there’s no doubt it is getting attention from competitors. The competition comes from two sources:

Major brands such as Nike, Hoka Clogs, and Adidas clogs

Counterfeit or no-name brands, shoes like Crocs on Amazon

There’s no doubt Crocs would face a lot of competition from both well-known brands and no-name brands. However, there are a couple of reasons I believe Crocs would maintain its competitive power.

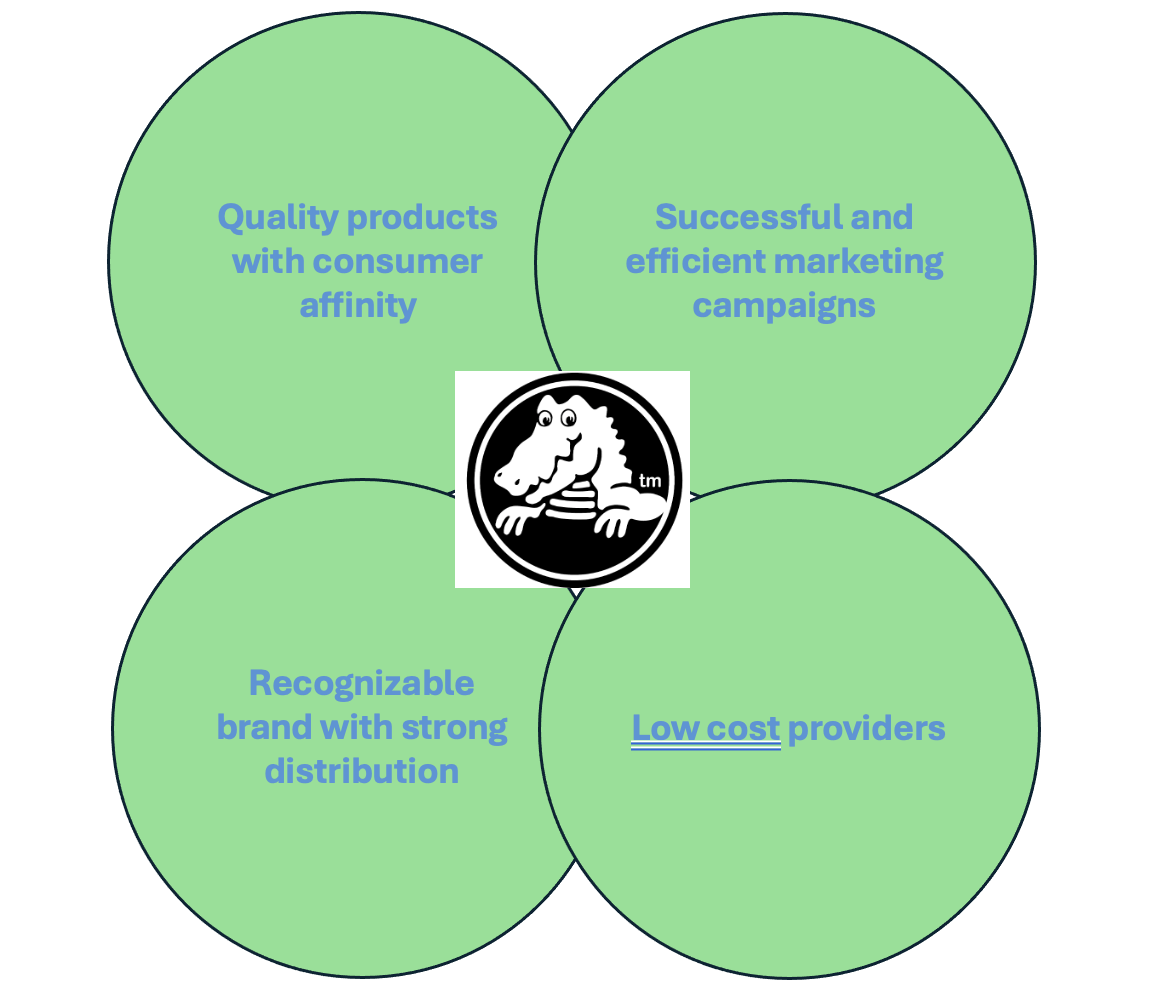

Crocs is the very few brands that share these four attributes at the same time:

Quality products with consumer affinity

Recognizable brands with strong distributions

Efficient & successful marketing campaigns

Low price offering, with its ASP (average sale price) less than $25 per pair, in large part due to the economies of scale.

I read a lot about Buffet’s investment in Coca-Cola and why he thought Coke was a great long-term bet in the late 80's. What Buffet saw at the time while others didn't was that Coke is the very few consumer brands that can command these four attributes above within one product. All four attributes are valuable for any brand and any company. But being able to combine all four in one is just a rare gem. In particular, being able to offer high-quality products while offering the lowest price is a very powerful moat against competition. There’s no doubt other companies can reproduce products that taste like Coke. But few could offer it at a cheaper price while maintaining profit. A well-established and recognizable brand also forms a distribution channel barrier for competitors to enter, especially before the Amazon era.

While Croc is by no means as dominant or comparable as what Coke was 30 years ago, I do see the many similarities between the two brands based on the four attributes listed above. Again, any one of these attributes is valuable to any brand. However, combining all four attributes into one forms a formidable barrier for competitors to cross.

For example, for well-known brands such as Nike and Adidas, clog shoes are in general at a higher price point. I am not sure if this is due to brand image or the lack of economic scale. After all, clogs are not the key focus of these large shoe makers like Nike or Adidas, whose key focus is sneakers and sports shoes. They are perhaps much more worried about the competition from other sneaker brands such as On and Hoka. To some extent, a good example of the innovators' dilemma.

For those less well-known brands, having a good distribution channel, especially offline, is a challenge to compete against Crocs. Amazon is the major distribution channel and battlefield. But again, the high quality plus low price point of Crocs shoes make it hard to compete against. It’s not impossible, but it’s just not as easy.

Growth

Crocs’s organic growth has slowed down dramatically after COVID-19, mainly due to the US market saturation. However, Crocs still managed to keep growing its top lines. During the most recent earnings release, the Crocs brand grew 8% YoY, driven by 15% YOY of international growth and 2% US growth. Currently, for the Crocs brand, the US accounts for about 57% of total revenue, and international accounts for 43%. With its current growth trajectory, international sales will exceed domestic sales in 2-3 years and still have a pretty long runway. Four countries are listed as its key strategic growth regions: China, India, Japan, and South Korea.

In addition to international growth, Crocs has a few other growth drivers. Growth is still a key focus area of the management and they put these strategic growth drivers on the first page of their annual reports. These five growth drivers below are listed on the first page under the vision session in its annual report.

Growing digital sales

Digital sales include sales directly to consumers through our company-owned websites and third-party marketplaces, as well as wholesale sales to our global e-tailers.

Gaining sandals market share for the Crocs Brand

Sandals have long been a focus of the Crocs Brand as a large and accessible growth avenue.

We believe sandals are a natural extension of the Crocs Brand, allowing us to access new consumers by leveraging our signature molding technology to provide casual, comfortable footwear for various occasions.

Increasing awareness and distribution for the HEYDUDE Brand

We have embarked on various marketing activities to drive higher awareness, including developing a pipeline of collaborations and brand activations.

We have right sized HEYDUDE’s wholesale distribution footprint and are evolving our channel diversification strategy through thoughtful outlet retail development.

In 2023, we opened 5 HEYDUDE Brand outlet stores.

Growth opportunities internationally

As a company with a well-established global footprint, we believe we have long-term sales growth opportunities internationally.

Our international sales in 2023 were 32.5% of consolidated revenues, compared to 29.4% in 2022 and 32.8% in 2021.

This includes sales for the HEYDUDE Brand, which operates primarily in the United States.

Our six core markets for the Crocs Brand include five international markets, specifically four markets in Asia: China, India, Japan, and South Korea.

Ongoing product and marketing innovation

At the heart of our Crocs Brand’s DNA are our clogs, sandals, and Jibbitz™ charms, which are key product pillars driving long-term growth.

We continue to grow our clog silhouette with new designs, colors, graphics, licensed images, embellishments, and accessories like Jibbitz™ charms for personalization.

The addition of the HEYDUDE Brand provides an innovative loafer concept that is differentiated through ease of use, quality, and comfort.

A few calls out here - Sandals have been a focus area of the Crocs and have had huge success. As an adjacent category, Sandals's revenue exceeded $400M early this year. That’s a very significant amount and accounts for nearly 15% of total Crocs revenue and is still growing. As the company shared, many families or consumers started trying Crocs’s sandals before its clogs, as it is less polarized than the “classic clogs”. Interestingly, that turns out to be true for our family. I first bought Crocs sandals for my kids and myself. Since then, we have been loyal to Crocs sandal customers.

Crocs Jibbitz has been growing fast and contributes to the personalization of the brand, especially for Asian markets in which there is higher adoption of Jibbitz and personalization. Crocs’s Jibbitz has generated $250M - $300M revenue and is still growing at double digits. Crocs doesn’t report Jibbitz as a business line, but I estimate that the gross margin of these little charms can easily go 80%-90% and the operating margin is like $50%. That is like a very successful software business that only needs a few designers to run.

Summary & End.

I recently read Howard Mark's The Most Important Thing again. Here is the quote that touches me the most.

There are two primary elements in superior investing

First, seeing some quality that others don’t see or appreciate, and that isn’t reflected in the price.

Second, having it turn out to be true.

There are very few companies that

I could understand and see more than the market does (have insight, or at least I have conviction that I do)

The business is high quality, measured by its business economics such as profit margins and ROIC, and its management quality

Having an attractive valuation with a margin of safety.

Nice post!